TORONTO, March 27, 2026 (GLOBE NEWSWIRE) — Hudbay Minerals Inc. (“Hudbay” or the “Company”) (TSX, NYSE: HBM) today released its annual mineral reserve and resource update and issued new three-year production guidance. All amounts are in U.S. dollars, unless otherwise noted.

- Affirmed 2026 production guidance and issued new 2027 and 2028 production guidance, demonstrating increased copper and strong gold production from Hudbay’s stable operating platform with three long-life operations in tier-one mining jurisdictions in the Americas.

- Consolidated copper production is expected to average 147,000i tonnes per year over the next three years, an increase of 24% from 2025 production. Consolidated copper production is expected to average 159,000i tonnes per year in 2027 and 2028, representing a 28% increase from expected 2026 production. This reflects the benefits from the expected completion of the optimization efforts at Copper Mountain and mill throughput improvement projects at Constancia in 2026.

- Strong complementary gold exposure with consolidated gold production expected to average 243,000i ounces per year over the next three years, reflecting continued strong production in Manitoba and the expected contribution from New Ingerbelle in British Columbia starting in 2028.

- Constancia’s expected mine life extends to 2040, reflecting higher mill throughput rates contributing to a 9% increase in expected average annual copper production to 90,000i tonnes per year in 2027 and 2028 from 2026 levels.

- Snow Lake’s expected mine life extended by four years to 2041, with average annual gold production of 190,000i ounces expected over the next three years from continued strong mill throughput rates at New Britannia.

- Copper Mountain’s expected mine life extended by two years to 2045, with significantly higher copper and gold production averaging 57,500i tonnes and 38,500i ounces, respectively, per year over 2027 and 2028, an increase of 92% and 43%, respectively, from 2026 levels. This increase reflects higher mill throughput, higher grades from completion of the accelerated stripping program in late 2026 and the expected contribution from New Ingerbelle starting in 2028.

- Large exploration program in Snow Lake continues to execute a threefold strategy focused on near-mine exploration to increase near-term production and mineral reserves, testing regional satellite deposits for additional ore feed to utilize available capacity at the Stall mill, and exploring the large land package for a potential new anchor deposit to meaningfully extend mine life.

- Definitive feasibility study at Copper World on track for completion in mid-2026 with a sanctioning decision expected in 2026. Closed the accretive $600 million joint venture transaction with Mitsubishi Corporation (“Mitsubishi”) in January 2026, securing a premier, long-term 30% strategic partner for the development of Copper World and achieving the key financial elements of the Company’s 3-P plan.

“Our updated mineral reserve estimates and three-year production outlook demonstrate Hudbay’s continued success from our exploration initiatives and an improved copper and gold production profile from our three long life operations in tier one mining jurisdictions in the Americas,” said Peter Kukielski, Hudbay’s President and Chief Executive Officer. “With our newly released guidance through 2028, consolidated copper production is expected to increase by 24%, complemented by continued strong gold exposure. This growth is underpinned by meaningful mine life extensions at Snow Lake and Copper Mountain reinforcing the longevity and upside of our operating base. As we embark on generational reinvestments across our business in exploration and brownfield growth opportunities, continue to advance Copper World toward a sanctioning decision in 2026, and integrate the Cactus project through the strategic acquisition of Arizona Sonoran, Hudbay is in an optimal position to deliver attractive high-return growth, significantly increase long-term copper exposure and unlock meaningful value for stakeholders.”

Constancia Operations

Constancia is Hudbay’s 100% owned copper operation located in the province of Chumbivilcas in southern Peru. The Pampacancha high-grade satellite deposit was mined between 2021 and 2025 and provided a significant source of higher-grade mill feed in recent years until mining activities were completed in the fourth quarter of 2025.

Current mineral reserve estimates total 488 million tonnes at 0.24% copper containing approximately 1.2 million tonnes of copper, after deducting 2025 mining depletion. The expected mine life of Constancia is now until 2040 as mill throughput rates are expected to increase to more than 90,000 tonnes per day starting in the second half of 2026 with the installation of two pebble crushers and related permit amendments. These initiatives are intended to optimize the utilization of existing infrastructure and support improved long-term operating performance.

In 2025, Hudbay optimized the mine plan during a period of social unrest by prioritizing Pampacancha mining activities and supplementing mill ore feed from low-grade stockpiles. Following the accelerated depletion of Pampacancha, mining activities at Pampacancha were completed in the fourth quarter of 2025. The remaining stockpiled Pampacancha ore was fully processed in early 2026 and the Company is now exclusively mining and processing ore from the Constancia deposit.

Annual production at the Constancia operations is expected to average approximately 87,500i tonnes of copper and 18,500i ounces of gold over the next three years. This reflects steady copper production levels as higher mill throughput is expected to offset lower grades starting in 2026 after the completion of mining at Pampacancha in late 2025.

Current mineral reserves and resources (exclusive of reserves) for Constancia and Pampacancha as of January 1, 2026 are summarized below.

| Constancia Operations Mineral Reserve and Resource Estimates1,2,3,4,5 |

Tonnes | Cu Grade (%) | Mo Grade (g/t) | Au Grade (g/t) | Ag Grade (g/t) | |

| Constancia Reserves | ||||||

| Proven | 458,800,000 | 0.243 | 75 | 0.036 | 2.39 | |

| Probable | 28,300,000 | 0.193 | 68 | 0.034 | 1.98 | |

| Total Proven and Probable – Constancia | 487,100,000 | 0.240 | 74 | 0.036 | 2.37 | |

| Pampacancha Reserves6 | ||||||

| Proven | 900,000 | 0.216 | 128 | 0.307 | 3.57 | |

| Probable | – | – | – | – | – | |

| Total Proven and Probable – Pampacancha | 900,000 | 0.216 | 128 | 0.307 | 3.57 | |

| Total Proven and Probable | 488,000,000 | 0.240 | 74 | 0.036 | 2.37 | |

| Constancia Resources | ||||||

| Measured | 106,300,000 | 0.232 | 74 | 0.036 | 2.36 | |

| Indicated | 70,400,000 | 0.222 | 87 | 0.032 | 2.00 | |

| Inferred – Open Pit | 27,700,000 | 0.271 | 71 | 0.049 | 2.54 | |

| Inferred – Underground | 6,500,000 | 1.200 | 69 | 0.140 | 8.62 | |

| Pampacancha Resources | ||||||

| Inferred | – | – | – | – | – | |

| Total Measured and Indicated | 176,700,000 | 0.228 | 79 | 0.034 | 2.22 | |

| Total Inferred | 34,200,000 | 0.447 | 71 | 0.067 | 3.70 | |

Note: totals may not add up correctly due to rounding.

1 Mineral resources are exclusive of mineral reserves and do not have demonstrated economic viability.

2 Mineral reserves are estimated using a minimum NSR cut-off of $7.30 per tonne at Pampacancha, $7.30 per tonne at Constancia and assuming metallurgical recoveries (applied by ore type) of 85.29% for copper on average for the life of mine.

3 Mineral resource estimates are based on resource pit design and do not include factors for mining recovery or dilution.

4 The open pit mineral resources are estimated using a minimum NSR cut-off of $7.30 per tonne and assuming metallurgical recoveries (applied by ore type) of 84.6% for copper on average for the life of mine, while the underground inferred resources at Constancia Norte are based on a 0.65% copper cut-off grade.

5 Long-term metal prices of $4.40 per pound copper, $17.00 per pound molybdenum, $2,800 per ounce gold and $32.00 per ounce silver were used to confirm the economic viability of the mineral reserve estimates and to estimate mineral resources.

6 There are no additional mineral resources left at Pampacancha where mining activities have been completed in 2025.

Snow Lake Operations

Hudbay’s 100% owned Snow Lake operations in Manitoba include the Lalor gold-copper-zinc mine, the New Britannia gold mill, the Stall base metals concentrator, the 1901 zinc-gold deposit and several satellite deposits. The Lalor mine achieved commercial production in 2014 and reached a significant milestone in December 2024 with the recovery of one million ounces of gold from the mine. In 2025, near-mine exploration at the Lalor mine was conducted and is expected to continue into 2026, with the objective of increasing mineral reserves and resources and supporting future production.

The 1901 deposit was discovered in 2019, and in 2020 and 2021 Hudbay conducted infill drilling, metallurgical testing and a pre-feasibility study at 1901. In 2025, an exploration drift was successfully completed to reach the 1901 mineralized zone in order to conduct exploration activities and establish critical infrastructure ahead of full production expected in late 2027.

Current mineral reserve estimates in Snow Lake total 19.6 million tonnes with approximately 1.9 million ounces of gold and an expected mine life to 2041. After adjusting for mining depletion, this represents an increase of approximately 330,000 ounces of gold and an additional four years of mine life. High grade resource to reserve conversions and re-evaluation gains have offset reductions related to the optimization of the mine plan through the removal of lower grade dilution and low value reserves requiring significant development.

Snow Lake’s life-of-mine production schedule has been optimized for higher mill throughput rates at New Britannia, maximizing gold production and cash flows. In 2025, the Snow Lake operations continued to deliver meaningful gold production despite operational disruptions, including two months of mandatory wildfire evacuations and a one-week power outage caused by a winter storm. The Snow Lake operations produced 173,453 ounces of gold in 2025 with the New Britannia mill continuing to perform strongly, achieving a new monthly throughput record of approximately 2,300 tonnes per day in December 2025.

Annual production at the Snow Lake operations is expected to average approximately 190,000i ounces of gold and 11,500i tonnes of copper over the next three years. This reflects continued strong gold production levels, with New Britannia mill throughput expected to continue to operate above 2,200 tonnes per day and Lalor operating at 4,000 to 4,500 tonnes per day, supplemented by contributions from the 1901 deposit ramp up.

Current mineral reserves and resources (exclusive of reserves) for Lalor, 1901 and other Snow Lake satellite deposits as of January 1, 2026 are summarized below.

| Lalor Mine and 1901 Deposit Mineral Reserve and Resource Estimates1,2,3,4,5,6,7 |

Tonnes | Au Grade (g/t) | Zn Grade (%) | Cu Grade (%) | Ag Grade (g/t) | |

| Gold Zone Reserves | ||||||

| Proven – Lalor | 4,800,000 | 4.28 | 0.70 | 0.51 | 27.0 | |

| Proven – 1901 | – | – | – | – | – | |

| Probable – Lalor | 4,900,000 | 3.41 | 0.27 | 0.87 | 16.8 | |

| Probable – 1901 | – | – | – | – | – | |

| Total Proven and Probable – Gold | 9,800,000 | 3.84 | 0.48 | 0.69 | 21.8 | |

| Base Metal Zone Reserves | ||||||

| Proven – Lalor | 4,400,000 | 2.42 | 4.36 | 0.36 | 27.7 | |

| Proven – 1901 | 900,000 | 2.25 | 7.60 | 0.27 | 24.0 | |

| Probable – Lalor | 600,000 | 1.50 | 4.11 | 0.34 | 25.1 | |

| Probable – 1901 | 700,000 | 1.67 | 8.23 | 0.22 | 28.5 | |

| Total Proven and Probable – Base Metal | 6,700,000 | 2.22 | 5.20 | 0.33 | 27.0 | |

| Total Gold and Base Metal Zone Reserves | ||||||

| Proven and Probable – Lalor | 14,800,000 | 3.31 | 1.80 | 0.58 | 23.7 | |

| Proven and Probable – 1901 | 1,600,000 | 1.99 | 7.89 | 0.24 | 26.0 | |

| Total Proven and Probable (Gold and Base Metal) | 16,500,000 | 3.18 | 2.40 | 0.54 | 23.9 | |

| Gold Zone Resources | ||||||

| Inferred – Lalor | 1,400,000 | 4.64 | 0.21 | 2.48 | 15.4 | |

| Inferred – 1901 | 2,700,000 | 4.20 | 0.65 | 0.58 | 16.3 | |

| Total Inferred – Gold | 4,100,000 | 4.35 | 0.50 | 1.24 | 16.0 | |

| Base Metal Zone Resources | ||||||

| Inferred – Lalor | 400,000 | 1.42 | 1.74 | 1.28 | 18.3 | |

| Inferred – 1901 | 100,000 | 1.23 | 8.12 | 0.13 | 38.1 | |

| Total Inferred – Base Metal | 500,000 | 1.37 | 3.39 | 0.98 | 23.4 | |

| Total Gold and Base Metal Zone Resources | ||||||

| Inferred – Lalor | 1,800,000 | 3.95 | 0.53 | 2.22 | 16.0 | |

| Inferred – 1901 | 2,800,000 | 4.06 | 1.01 | 0.56 | 17.3 | |

| Total Inferred (Gold and Base Metal) | 4,600,000 | 4.02 | 0.82 | 1.21 | 16.8 | |

Note: totals may not add up correctly due to rounding.

1 Mineral resources are exclusive of mineral reserves and do not have demonstrated economic viability.

2 Lalor mineral reserves and resources are estimated using a NSR cut-off ranging from C$161 to C$185 per tonne, assuming a long hole mining method and depending on mill destination.

3 Individual stope gold grades at Lalor and 1901 were capped at 10 grams per tonne.

4 1901 mineral reserves and resources are estimated using a minimum NSR cut-off of C$199 per tonne.

5 Mineral resources do not include factors for mining recovery or dilution.

6 Base metal mineral resources are estimated based on the assumption that they would be processed at the Stall concentrator while gold mineral resources are estimated based on the assumption that they would be processed at the New Britannia concentrator.

7 Long-term metal prices of $2,800 per ounce gold, $1.25 per pound zinc, $4.40 per pound copper and $32.00 per ounce silver with an exchange rate of 1.33 C$/US$ were used to confirm the economic viability of the mineral reserve estimates and to estimate mineral resources.

| Snow Lake Regional Deposits – Gold Mineral Reserve and Resource Estimates1,2,3,4,5,6,7 |

Tonnes | Au Grade (g/t) | Zn Grade (%) | Cu Grade (%) | Ag Grade (g/t) | |

| Probable Reserves | ||||||

| WIM | 2,450,000 | 1.6 | 0.25 | 1.63 | 6.3 | |

| 3 Zone | 660,000 | 4.2 | – | – | – | |

| Total Probable (Gold) | 3,110,000 | 2.2 | 0.20 | 1.28 | 5.0 | |

| Inferred Resources | ||||||

| New Britannia | 2,750,000 | 4.5 | – | – | – | |

| Birch | 570,000 | 4.4 | – | – | – | |

| Total Inferred (Gold) | 3,320,000 | 4.5 | – | – | – | |

Note: totals may not add up correctly due to rounding.

1 Mineral resources are exclusive of mineral reserves and do not have demonstrated economic viability.

2 WIM mineral reserves assume processing recoveries of 98% for copper, 88% for gold, and 70% for silver based on processing through New Britannia’s flotation and tails leach circuits.

3 3 Zone mineral reserves assume processing recoveries of 85% for gold based on processing through New Britannia’s leach circuit.

4 Long-term metal prices of $1,700 per ounce gold, $1.25 per pound zinc, $4.00 per pound copper and $23.00 per ounce silver with an exchange rate of 1.33 C$/US$ were used to confirm the economic viability of the mineral reserve estimates.

5 Mineral resources do not include factors for mining recovery or dilution.

6 Gold mineral resources are estimated based on the assumption that they would be processed at the New Britannia concentrator.

7 New Britannia mineral resource estimates have been reported at a minimum true width of 1.5 metres and with a cut-off grade varying from 2 grams per tonne (at the lower part of New Britannia) to 3.5 grams per tonne (at the upper part of New Britannia).

| Snow Lake Regional Deposits – Base Metal Mineral Reserve and Resource Estimates1,2,3,4,5,6,7 |

Tonnes | Au Grade (g/t) | Zn Grade (%) | Cu Grade (%) | Ag Grade (g/t) | |

| Indicated Resources | ||||||

| Pen II | 470,000 | 0.3 | 8.89 | 0.49 | 6.8 | |

| Talbot | 2,190,000 | 2.1 | 1.79 | 2.33 | 36.0 | |

| Total Indicated (Base Metals) | 2,660,000 | 1.8 | 3.04 | 2.01 | 30.9 | |

| Inferred Resources | ||||||

| Watts | 3,150,000 | 1.0 | 2.58 | 2.34 | 31.0 | |

| Pen II | 130,000 | 0.3 | 9.81 | 0.37 | 6.8 | |

| Talbot | 2,450,000 | 1.9 | 1.74 | 1.13 | 25.8 | |

| Total Inferred (Base Metals) | 5,730,000 | 1.3 | 2.39 | 1.78 | 28.3 | |

Note: totals may not add up correctly due to rounding.

1 Mineral resources are exclusive of mineral reserves and do not have demonstrated economic viability.

2 Mineral resources do not include factors for mining recovery or dilution.

3 Base metal mineral resources are estimated based on the assumption that they would be processed at the Stall concentrator.

4 Watts and Pen II mineral resources were initially estimated using metal price assumptions that vary marginally over the assumptions used to estimate mineral resources at Lalor. In the Qualified Person’s opinion, the combined impact of these small variations does not have any impact on the mineral resource estimates.

5 Watts mineral resources are estimated using a minimum NSR cut-off of C$150 per tonne, assuming processing recoveries of 90% for copper, 80% for zinc, 70% for gold and 70% for silver.

6 Pen II mineral resources are estimated using a minimum NSR cut-off of C$75 per tonne.

7 The above resource estimates table includes 100% of the Talbot mineral resources reported by Rockcliff Metals Corp. in its 2020 NI 43-101 technical report published on SEDAR+.

Snow Lake Exploration Program – Executing Threefold Strategy

Hudbay continues to execute an extensive exploration program in Snow Lake through geophysical surveying and multi-phased drilling campaigns as part of its threefold exploration strategy.

1) Near-Mine Exploration to Further Increase Near-term Production and Extend Mine Life

Near-mine exploration at the Lalor mine and the adjacent 1901 deposit continued to support near-term production growth and mine life extension. The exploration program will continue into 2026 to potentially increase mineral reserves and resources and enable resource conversion.

The Company completed development of the initial exploration drift at the 1901 deposit in 2025 and commenced delivery of zinc-rich development ore for processing at Stall. Activities at the 1901 deposit over the next two years will focus on exploration and definition drilling, orebody access and establishing the critical infrastructure required to support full production beginning in late 2027. Exploration activities will include step-out drilling to potentially extend the orebody, as well as infill drilling aimed at converting inferred mineral resources within the gold lenses to mineral reserves.

2) Testing Regional Satellite Deposits to Utilize Available Processing Capacity and Increase Production

Hudbay increased its land package in Snow Lake by more than 250% through the acquisition of Rockcliff Metals Corp. (“Rockcliff”) in 2023, which included the addition of several known deposits located within trucking distance of the Snow Lake processing infrastructure. These former Rockcliff deposits, together with several deposits already owned by Hudbay, have created an attractive portfolio of regional deposits in Snow Lake, including the Talbot, New Britannia, Rail, Pen II, Watts, 3 Zone and WIM deposits. The continued strong performance from the New Britannia mill has freed up additional processing capacity at the Stall mill, where there is approximately 1,500 tonnes per day of available capacity which could be utilized by the regional satellite deposits to potentially increase production and extend the life of the Snow Lake operations beyond 2041.

The above-mentioned properties are shown in Figure 1, and includes:

- Talbot – Consolidated 100% ownership of this copper-zinc-gold rich deposit through Hudbay’s acquisition of Rockcliff in 2023. Rockcliff estimated indicated mineral resources of 2.2 million tonnes at 2.3% copper, 1.8% zinc and 2.1 grams per tonne gold.

- New Britannia – Acquired by Hudbay in 2015 with the acquisition of the New Britannia gold mill, the New Britannia deposit is a former producing gold mine that produced approximately 600,000 ounces between 1949 and 1958 and an additional 800,000 ounces between 1995 and 2005. Significant mineral resources remain accessible at New Britannia and the Company is advancing plans on potential future development and rehabilitation of the existing mining infrastructure at New Britannia to unlock significant incremental gold production in Snow Lake.

- Rail – Also acquired as part of Hudbay’s acquisition of Rockcliff in 2023, Hudbay’s 2024 drill program yielded new intersections of high-grade copper-gold mineralization. These results will be combined with historical drilling results on the property to update the geological model and assess its economic potential.

- Pen II – Hudbay consolidated land adjacent to this low tonnage, near surface, high-grade zinc deposit through the Rockcliff acquisition. Rockcliff intersected mineralization down-dip from Hudbay’s deposit and identified a deep geophysical conductive plate.

- Watts – A copper-zinc-rich deposit located near powerlines and 100 kilometres by road from the Stall mill. Drilling by Hudbay in 2019 successfully extended the known high-grade copper mineralization.

- 3 Zone – Acquired by Hudbay in 2015, this gold-rich deposit is located three kilometres from the New Britannia mill and is expected come into production after the Lalor deposit is depleted.

- WIM – Acquired by Hudbay in 2018, this copper-gold deposit is located 15 kilometres from the New Britannia mill and is expected to come into production after the Lalor deposit is depleted.

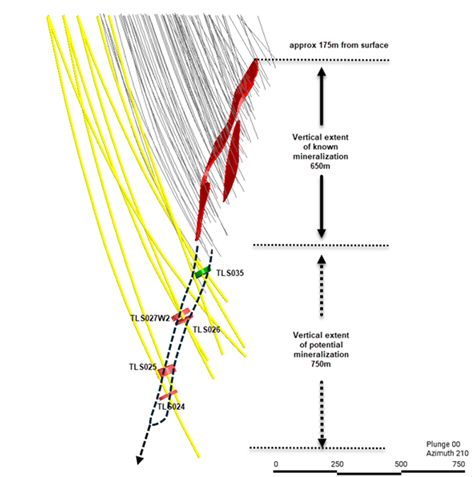

Talbot Initial Drill Results Confirm Resource Expansion Potential

Talbot is a copper-zinc-gold rich volcanogenic massive sulfide (“VMS”) deposit located within trucking distance of existing processing infrastructure in Snow Lake. Successful drilling campaigns are expected to expand the resource base and support a pre-feasibility study (“PFS”) aimed at upgrading mineral resources to mineral reserves and extending the overall mine life of the Snow Lake operations. In April 2025, Hudbay announced the signing of an exploration agreement with the Mosakahiken Cree Nation covering exploration activities within their traditional and ancestral territory, including at Talbot.

In July 2025, Hudbay commenced an extensive summer drilling program at Talbot focused on expanding the known mineralization at depth, testing geophysical targets and conducting an infill drill program in the upper portion of the orebody to support the PFS, as seen in Figure 2. As part of the initial drilling program in 2025, Hudbay drilled five holes to test the continuity of the Talbot deposit at depth, with all holes intersecting intervals of copper mineralization including 2.4% copper and 1.8 grams per tonne gold over 10.4 metres. In addition, another hole intersected copper mineralization over an estimated length of 19.7 metres based on core logging, for which assay results are pending.

The 2026 drilling program will continue with an expanded fleet of eight drill rigs deployed to test additional targets and expand the footprint of the deposit at depth. The efforts will determine the future scope of a PFS including shaft versus ramp access and the best location for a future exploration shaft. Hudbay intends to update Rockcliff’s prior mineral resource estimate for Talbot using Hudbay’s standard methods that have demonstrated high mineral reserve conversion rates.

3) Exploring Large Land Package for New Anchor Deposit to Significantly Extend Mine Life

A majority of the land claims acquired as part of the Rockcliff acquisition in 2023 have been untested by modern deep geophysics, which was the discovery method for the Lalor deposit. A large geophysics program is currently underway consisting of surface electromagnetic surveys using cutting edge techniques that enable the team to detect targets at depths of almost 1,000 metres below surface. The planned geophysics program includes 600 kilometres of ground electromagnetic surveys and an extensive airborne geophysics survey. Over the past two years, Hudbay has progressed the geophysics program mapping, as seen in Figure 1, which will continue in 2026 with the outlined regions of focus.

Expanded Flin Flon Exploration Partnership with Marubeni and JOGMEC

On January 22, 2026, the Company announced the signing of an amended and restated option agreement with Japan Organization for Metals and Energy Security (“JOGMEC”) and Marubeni Corporation (“Marubeni”), where Hudbay granted JOGMEC an option to acquire a 10% interest in three projects located within trucking distance of Hudbay’s processing facilities in Flin Flon, Manitoba. In order to exercise its option, JOGMEC is required to fund at least C$6 million in exploration expenditures over a period of approximately three years, with Hudbay acting as the operator carrying out the exploration activities. The agreement is an amendment and restatement of the option agreement with Marubeni from March 2024, pursuant to which Marubeni’s wholly-owned Canadian subsidiary was granted an option to acquire a 20% interest in the three projects, provided it, funds at least C$12 million in exploration expenditures over the designated earn-in period, which is inclusive of past contributions made by Marubeni since March 2024.

The option agreement focuses on three projects in the Flin Flon region, namely Cuprus-White Lake, Westarm and North Star, which were selected by Marubeni prior to the original March 2024 agreement and following a period of detailed due diligence. All three properties hold past producing mines that generated meaningful production with attractive grades of both base metals and precious metals. The properties remain highly prospective with potential for further discovery based on the attractive geological setting, limited historical deep drilling and promising geochemical and geophysical targets. Cuprus-White Lake, Westarm and North Star are all within 20 kilometres of Hudbay’s Flin Flon milling complex.

Copper Mountain Mine

Hudbay’s 100% owned Copper Mountain mine is an open pit copper mine in southern British Columbia, which also produces gold and silver as by-product metals. Hudbay initially acquired a 75% interest in Copper Mountain as part of its acquisition of Copper Mountain Mining Corporation in June 2023, with Mitsubishi Materials Corporation (“MMC”) holding the remaining 25% minority interest. In April 2025, Hudbay acquired MMC’s 25% minority interest and, as a result, Hudbay now holds a 100% interest in the Copper Mountain mine.

Current mineral reserve estimates at Copper Mountain total 345 million tonnes at 0.26% copper and 0.12 grams per tonne gold, containing approximately 883 thousand tonnes of copper and 1.3 million ounces of gold. These mineral reserves support a mine life until 2045, representing an extension of two years, with additional upside potential for future resource conversion and mine life extension through 122 million tonnes of measured and indicated resources grading 0.21% copper and 0.10 grams per tonne gold and 347 million tonnes of inferred resources grading 0.24% copper and 0.12 grams per tonne gold, in each case exclusive of mineral reserves. Post 2025 mining depletion, the mineral reserve estimates have slightly improved in both tonnes and grade due to the addition of approximately 15 million tonnes at New Ingerbelle, driven by an optimized pit design and the substitution of low-grade mineralization with higher grade ore identified during the 2025 infill program. 2026 drilling activities will focus on the continued conversion of high value inferred resources at New Ingerbelle to potentially further extend mine life at Copper Mountain.

Since acquiring Copper Mountain in June 2023, Hudbay has focused on advancing operational optimization and stabilization initiatives at the mine, including reactivating the full mining fleet, adding additional haul trucks, opening additional mining faces, optimizing ore feed to the plant and implementing plant improvement initiatives that mirror Hudbay’s successful processes at Constancia.

In 2025, the conversion of the third ball mill to a second SAG mill was substantially completed and the permanent feeder configuration was commissioned in December 2025. A feed-end head replacement for the primary SAG mill is planned for mid-2026. Mill throughput is expected to ramp toward its permitted capacity of 50,000 tonnes per day in the second half of the year.

In February 2026, amended permits were received for the New Ingerbelle expansion project, supporting continued copper production, increased gold production and future mine life extension potential from the New Ingerbelle satellite pit. The expansion is designed to access higher-grade mineralization while improving operational efficiency with a stripping ratio approximately three times lower than current mining areas. In parallel, Hudbay also refreshed Participation Agreements with the Upper Similkameen Indian Band (“USIB”) and Lower Similkameen Indian Band (“LSIB”) in February 2026.

These developments support Hudbay’s continued efforts to stabilize and optimize operations at Copper Mountain and position the British Columbia operations to contribute to strong consolidated copper production as Copper Mountain continues to ramp up. Annual production at the British Columbia operations is expected to average approximately 48,000i tonnes of copper and 35,000 ounces of gold over the next three years.

Current mineral reserves and resources (exclusive of reserves) for Copper Mountain as of January 1, 2026 are summarized below.

| Copper Mountain Mine Mineral Reserve and Resource Estimates1,2,3,4,5 |

Tonnes | Cu Grade (%) |

Au Grade (g/t) |

Ag Grade (g/t) |

|

| Reserves | |||||

| Proven | 159,000,000 | 0.251 | 0.111 | 0.71 | |

| Probable | 186,000,000 | 0.260 | 0.133 | 0.60 | |

| Total Proven and Probable | 345,000,000 | 0.256 | 0.123 | 0.65 | |

| Resources | |||||

| Measured | 35,000,000 | 0.226 | 0.086 | 0.83 | |

| Indicated | 87,000,000 | 0.203 | 0.101 | 0.72 | |

| Measured and Indicated | 122,000,000 | 0.210 | 0.097 | 0.75 | |

| Inferred | 347,000,000 | 0.235 | 0.124 | 0.57 | |

Note: totals may not add up correctly due to rounding.

1 Mineral resource estimates are exclusive of mineral reserves. Mineral resources are not mineral reserves as they do not have demonstrated economic viability. Mineral reserves and resources include Copper Mountain and New Ingerbelle deposits.

2 Mineral reserves are estimated using a 0.1% copper cut-off grade and assuming metallurgical recoveries (applied by ore type) of 87% for copper for New Ingerbelle, 85% copper for Copper Mountain, 70% for gold for New Ingerbelle, 65% for gold for Copper Mountain and 70% for silver for both deposits throughout the life of mine.

3 Long term metal prices of $4.40 per pound copper, $2,800 per ounce gold and $32.00 per ounce silver were used to confirm the economic viability of the mineral reserve estimates and to estimate mineral resources.

4 Mineral resource estimate tonnes and grades constrained to a Lerch Grossman revenue factor 1 pit shell, post mining depletion.

5 Mineral resources are estimated using 0.1% copper cut-off grade.

3-Year Production Outlook

Hudbay has affirmed its 2026 production guidance as issued on February 20, 2026, and has issued new 2027 and 2028 production guidance in connection with updated life-of-mine models to support annual reserve and resource estimates. Consolidated copper production over the next three years is expected to average 147,000i tonnes, representing an increase of 24% from 2025 levels. 2027 and 2028 consolidated copper production is expected to average 159,000 tonnes per year, a 28% increase from 2026 expected consolidated copper production of 124,000 tonnes. The increase is due to higher expected copper production in British Columbia as a result of mill throughput ramping up to the targeted 50,000 tonnes per day in the second half of 2026, higher grades British Columbia in 2027 from the completing of the accelerated stripping schedule, and higher expected mill throughput in Peru from the addition of two pebble crushers and operating efficiencies in the second half of 2026. Consolidated gold production over the next three years is expected to average 243,000i ounces per year, representing a decrease of 9% from 2025 levels after the depletion of the high-grade Pampacancha satellite deposit in December 2025 but an increase in unstreamed higher-valued gold production in Manitoba. Continued strong gold production levels are expected to be driven by New Britannia mill throughput continuing to exceed expectations operating above 2,200 tonnes per operating day and the contribution from New Ingerbelle in 2028.

Peru’s three-year copper production guidance reflects stable copper production averaging 87,500i tonnes per year, as the depletion of Pampacancha in 2025 is offset by higher mill throughput and operating efficiencies. Peru expects to install two pebble crushers to increase mill throughput in the second half of 2026, in addition to implementing other mill optimization initiatives. 2027 and 2028 copper production is expected to be 90,000i tonnes, a 9% increase from 2026 expected copper production of 82,500 tonnes, benefiting from a full year of increased mill throughput and operating efficiencies and mine plan optimization to smooth copper production over the three-year period. The benefits of the mine plan optimization initiatives extend beyond the 3-year outlook with 2029 copper production expected to continue near these levels. Gold production over the next three years is expected to average 18,500i ounces, lower than 2025 levels as Hudbay accelerated the depletion of the high-grade Pampacancha satellite deposit in December 2025.

Manitoba’s three-year production guidance reflects continued strong gold production levels averaging 190,000i ounces per year. New Britannia mill throughput is expected to continue to exceed expectations and operate above 2,200 tonnes per day, far exceeding its original design capacity of 1,500 tonnes per day. The production guidance anticipates Lalor operating between 4,000 to 4,500 tonnes per day, supplemented by contributions from the 1901 deposit with a ramp up to 1,000 tonnes per day by 2028. In 2026, Hudbay expects to complete a feasibility study on the Stall mill tailings leaching project, which has the potential to further increase gold production starting in 2028. The benefits of this project have not been reflected in the production guidance. Zinc production is expected to increase to 32,500i tonnes by 2028, a 76% increase from 2026 and 2027 expected zinc production of 18,500i tonnes, driven by higher production from the 1901 deposit.

British Columbia’s three-year copper production guidance reflects sequentially higher copper production averaging 48,000i tonnes per year, as a result of the completion of the conversion of the third ball mill to second SAG mill in late 2025, installation of the replacement feed-end head at the primary SAG mill in the third quarter of 2026, and higher grades from the completion of the accelerated stripping program in 2026. 2027 and 2028 copper production is expected to average 57,500i tonnes, almost double 2026 expected copper production of 30,000i tonnes, benefiting from a full year of mill throughput at the targeted 50,000 tonnes per day and the unlocking of higher grades from the accelerated stripping program. Similarly, gold production over the next three years reflects sequentially higher production with average annual gold production of 38,500i ounces over 2027 and 2028, representing a 43% increase from 2026 as a result of the expected contribution from New Ingerbelle starting in 2028.

| 3-Year Production Outlook Contained Metal in Concentrate and Doré1 |

2026 Guidance | 2027 Guidance | 2028 Guidance | ||

| Peru | |||||

| Copper | tonnes | 75,000 – 90,000 | 80,000 – 100,000 | 80,000 – 100,000 | |

| Gold | ounces | 15,000 – 20,000 | 17,000 – 21,000 | 17,000 – 21,000 | |

| Silver | ounces | 1,900,000 – 2,400,000 | 1,200,000 – 1,400,000 | 2,000,000 – 2,500,000 | |

| Molybdenum | tonnes | 900 – 1,100 | 1,100 – 1,400 | 500 – 700 | |

| Manitoba | |||||

| Gold | ounces | 180,000 – 220,000 | 170,000 – 210,000 | 160,000 – 200,000 | |

| Zinc | tonnes | 16,000 – 21,000 | 16,000 – 21,000 | 29,000 – 36,000 | |

| Copper | tonnes | 10,000 – 13,000 | 10,000 – 14,000 | 9,000 – 13,000 | |

| Silver | ounces | 800,000 – 1,000,000 | 950,000 – 1,200,000 | 1,000,000 – 1,300,000 | |

| British Columbia | |||||

| Copper | tonnes | 25,000 – 35,000 | 50,000 – 70,000 | 50,000 – 60,000 | |

| Gold | ounces | 22,000 – 32,000 | 26,000 – 38,000 | 38,000 – 52,000 | |

| Silver | ounces | 200,000 – 290,000 | 500,000 – 660,000 | 420,000 – 580,000 | |

| Total | |||||

| Copper | tonnes | 110,000 – 138,000 | 140,000 – 184,000 | 139,000 – 173,000 | |

| Gold | ounces | 217,000 – 272,000 | 213,000 – 269,000 | 215,000 – 273,000 | |

| Zinc | tonnes | 16,000 – 21,000 | 16,000 – 21,000 | 29,000 – 36,000 | |

| Silver | ounces | 2,900,000 – 3,690,000 | 2,650,000 – 3,260,000 | 3,420,000 – 4,380,000 | |

| Molybdenum | tonnes | 900 – 1,100 | 1,100 – 1,400 | 500 – 700 | |

| 1 Metal reported in concentrate and doré is prior to smelting and refining losses or deductions associated with smelter terms. | |||||

Copper World Project

Copper World is a copper development project located in Pima County, Arizona, approximately 50 kilometres southeast of Tucson. Following completion of the Copper World joint venture transaction with Mitsubishi in January 2026 (the “JV Transaction”), Hudbay holds a 70% interest in Copper World LLC, which owns the Copper World project, with Mitsubishi holding the remaining 30% minority interest.

The Copper World project includes the large East deposit (formerly known as the Rosemont deposit) together with new deposits that were defined after the completion of an expanded drill program following a successful initial drill program in 2020. A new resource model was completed for the preliminary economic assessment (“PEA”) of Copper World in 2022, which contemplated a two-phased mine plan with Phase I as a standalone operation requiring state and local permits only and Phase II expanding onto federal lands requiring federal permits. In September 2023, Hudbay released its enhanced PFS for Copper World reflecting the results of further technical work on Phase I of the project. Hudbay received all three key state permits required for Copper World development and operation including the Mine Land Reclamation Plan initially approved in October 2021 and subsequently amended and approved in May 2023, the Aquifer Protection Permit received in August 2024, and the Air Quality Permit received in January 2025.

Copper World has an initial mine life of 20 years and is one of the highest-grade open pit copper projects in the Americas with proven and probable mineral reserves of 385 million tonnes at 0.54% copper. Based on the PFS, Phase I contemplates average annual copper production of 85,000 tonnes, at average cash costsii and sustaining cash costsii of $1.47 and $1.81 per pound of copper, respectively. At a copper price of $3.75 per pound and based on other assumptions in the PFS, the after-tax net present value (“NPV”) of Phase I using an 8% discount rate is $1.1 billion and the internal rate of return (“IRR”) is 19%. The valuation metrics are leveraged to higher copper prices and at a price of $4.25 per pound (without adjusting any other PFS assumptions), the after-tax NPV (8%) of Phase I increases to $1.7 billion, and the IRR increases to 25.5%.

There remains approximately 60% of the total copper contained in measured and indicated mineral resources (exclusive of mineral reserves), providing significant potential for Phase II expansion and mine life extension. In addition, the inferred mineral resource estimates are at a comparable copper grade and provide significant upside potential.

The Company took the following steps in 2025 and early 2026 to de-risk Copper World ahead of a sanction decision expected later this year:

- Realized Accretive JV Transaction – In January 2026, Hudbay announced the closing of the highly accretive $600 million JV Transaction, which represents a significant de-risking milestone in advancing Copper World and further validates the premium long-term value of this world-class asset. The $420 million of proceeds received at closing from Mitsubishi will be used to directly fund the remaining definitive feasibility study (“DFS”) costs and pre-sanctioning costs in addition to the initial project development costs for Copper World. Mitsubishi will contribute an additional $180 million within 18 months of closing to complete its 30% minority investment and will also fund its pro-rata 30% share of future equity capital contributions. The JV Transaction increases the project IRR to Hudbay to approximately 90% based on PFS estimates.

- Secured Premier Strategic Joint Venture Partner – Mitsubishi is one of the largest Japanese trading houses with a global mining presence and a significant U.S.-based business. Mitsubishi is the partner of choice with investments in a world-class portfolio of large and high-quality copper assets, including five of the top twenty copper mines globally by 2024 production. This partnership validates the attractive long-term value of Copper World as a world-class copper asset and endorses the strong technical capabilities of Hudbay. It also represents the beginning of a long-term strategic partnership, and the parties are identifying other opportunities for collaboration to advance their respective copper growth strategies.

- Achieved Key Financial Elements of Hudbay’s Three Prerequisites (3-P) Plan – Hudbay has achieved the final key financial elements of its prudent 3-P financial strategy for the development of Copper World with the closing of the JV Transaction and the achievement of stated balance sheet targets. After accounting for proceeds from the JV Transaction, Hudbay has post-closing cash and cash equivalents of $992 millioniii and reduced its post-closing net debt to adjusted EBITDA ratio to 0.0x, far exceeding the stated balance sheet targets. The Mitsubishi initial investment and its future pro-rata equity capital contributions, together with the Wheaton Precious Metals Corp. streamiv, provide significant financial flexibility by reducing Hudbay’s estimated share of the remaining capital contributions to approximately $200 million based on PFS estimates and deferring Hudbay’s first capital contribution to 2028 at the earliest.

- Feasibility Study and Detailed Engineering Underway – Feasibility activities for Copper World are well underway with expected completion of the DFS in mid-2026. Hudbay has continued to execute detailed engineering work and other de-risking activities, in preparation for a Copper World sanctioning decision expected in 2026.

Current mineral reserves and resources (exclusive of reserves) for the Copper World project as of January 1, 2026 are summarized below.

| Copper World Project Mineral Reserve and Resource Estimates1,2,3,4,5,6,7,8 |

Tonnes | Cu Grade (%) | Soluble Cu Grade (%) | Mo Grade (g/t) | Au Grade (g/t) | Ag Grade (g/t) |

| Reserves | ||||||

| Proven | 319,000,000 | 0.54 | 0.11 | 110 | 0.03 | 5.7 |

| Probable | 66,000,000 | 0.52 | 0.14 | 96 | 0.02 | 4.3 |

| Total Proven and Probable Reserves | 385,000,000 | 0.54 | 0.12 | 108 | 0.02 | 5.4 |

| Resources – Flotation | ||||||

| Measured | 424,000,000 | 0.39 | 0.04 | 150 | 0.02 | 4.1 |

| Indicated | 191,000,000 | 0.36 | 0.06 | 125 | 0.02 | 3.5 |

| Total Measured and Indicated (Flotation) | 615,000,000 | 0.38 | 0.05 | 142 | 0.02 | 3.9 |

| Inferred | 192,000,000 | 0.35 | 0.07 | 117 | 0.01 | 3.1 |

| Resources – Leach | ||||||

| Measured | 159,000,000 | 0.28 | 0.20 | – | – | – |

| Indicated | 70,000,000 | 0.26 | 0.20 | – | – | – |

| Total Measured and Indicated (Leach) | 229,000,000 | 0.27 | 0.20 | – | – | – |

| Inferred | 83,000,000 | 0.26 | 0.19 | – | – | – |

| Total Measured and Indicated | 844,000,000 | 0.35 | 0.09 | 104 | 0.01 | 2.9 |

| Total Inferred | 275,000,000 | 0.32 | 0.11 | 82 | 0.01 | 2.2 |

Note: totals may not add up correctly due to rounding.

1 Mineral resource estimates are exclusive of mineral reserves. CIM definitions were followed for the estimation of mineral resources. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

2 Long term metal prices of $4.00 per pound copper, $12.00 per pound molybdenum, $1,700 per ounce gold and $23.00 per ounce silver were used to confirm the economic viability of the mineral reserve estimates.

3 Mineral reserve estimates are limited to the portion of the measured and indicated resource estimates scheduled for milling and included in the financial model of the Copper World PFS.

4 Long-term metals prices of $3.75 per pound copper, $12.00 per pound molybdenum, $1,650 per ounce gold and $22.00 per ounce silver were used to estimate mineral resources.

5 Mineral resources are constrained within a computer-generated pit using the Lerchs-Grossman algorithm.

6 Mineral resource estimates were reported using a 0.1% copper cut-off grade and an oxidation ratio lower than 50% for flotation material and a 0.1% soluble copper cut-off grade and an oxidation ratio higher than 50% for leach material.

7 Estimate of the mineral reserve does not account for marginal amounts of historical small-scale operations in the area that occurred between 1870 and 1970 and is estimated to have extracted approximately 200,000 tonnes, which is within rounding approximations of the current reserve estimates.

8 Mineral reserve and resource estimates are presented on a 100% basis. Hudbay holds a 70% interest in the Copper World project following the completion of the Copper World joint venture transaction with Mitsubishi in January 2026.

Mason Project

The Mason project is a 100% owned greenfield copper deposit located in the historic Yerington District of Nevada and is one of the largest undeveloped copper porphyry deposits in North America. The Mason project’s measured and indicated mineral resources are comparable in size to Constancia. Hudbay views the Mason project as a long-term future development asset as part of the Company’s pipeline of high-quality copper growth opportunities. Since acquiring Mason, Hudbay has consolidated a prospective package of patented and unpatented mining claims contiguous to the Mason project and has advanced a number of technical studies, including a revised resource model and the completion of a PEA on Mason.

The Mason PEA was completed in 2021 and contemplates a 27-year mine life with average annual copper production of approximately 140,000 tonnes over the first ten years of full production. At a copper price of $4.00 per pound and based on the assumptions in the Mason PEA, the after-tax net present value using a 10% discount rate is $2.0 billion and the internal rate of return is 23%. For information regarding the limitations of a PEA, please refer to the Qualified Person and NI 43-101 statement at the end of this news release.

Since 2021, the Company has completed exploration activities at Mason, while continuing to focus on local stakeholder engagement. The Company is advancing additional metallurgical studies with the objective of further enhancing the project economics and plans to initiate a PFS for the Mason project in 2026.

Current mineral resource estimates for Mason as of January 1, 2026 are summarized below.

| Mason Project Mineral Resource Estimates1,2,3,4,5 |

Tonnes | Cu Grade (%) |

Mo Grade (g/t) |

Au Grade (g/t) |

Ag Grade (g/t) |

|

| Measured | 1,417,000,000 | 0.29 | 59 | 0.031 | 0.66 | |

| Indicated | 801,000,000 | 0.30 | 80 | 0.025 | 0.57 | |

| Total Measured and Indicated | 2,219,000,000 | 0.29 | 67 | 0.029 | 0.63 | |

| Inferred | 237,000,000 | 0.24 | 78 | 0.033 | 0.73 | |

Note: totals may not add up correctly due to rounding.

1 Mineral resource estimates that are not mineral reserves do not have demonstrated economic viability.

2 Mineral resource estimates do not include factors for mining recovery or dilution.

3 Metal prices of $3.10 per pound copper, $11.00 per pound molybdenum, $1,500 per ounce gold, and $18.00 per ounce silver were used to estimate mineral resources.

4 Mineral resources are estimated using a minimum NSR cut-off of $6.25 per tonne.

5 Mineral resources are based on resource pit designs containing measured, indicated, and inferred mineral resources.

Llaguen Project

The Llaguen project is a 100% owned copper-molybdenum porphyry deposit located near the city of Trujillo, the third largest city in Peru. Llaguen is at moderate altitude and in close proximity to existing infrastructure, water and power supply, including the port of Salaverry located 62 kilometres away and the Trujillo Nueva electric power substation located 40 kilometres away. Hudbay completed a 28-hole confirmatory drill program in 2021 and 2022, which confirmed and extended the footprint of the known mineralization and highlighted the existence of a high-grade zone in the center of the deposit.

After completing an initial mineral resource estimate in November 2022, Hudbay initiated preliminary technical studies, including metallurgical test work as well as geotechnical and hydrogeological studies, which are expected to be incorporated into a preliminary economic assessment for the Llaguen project. Additional exploration drilling is warranted on the Llaguen property to test the areas of the deposit that remain open and the several untested geophysical targets in the area to fully define the regional extent of the mineralization. The current mineral resource is also surrounded by a large halo of low grade hypogene copper mineralization, not currently included in the mineral resource estimate, but for which metallurgical test work could assess the potential for economic sulfide heap leaching via commercially available technologies.

Current mineral resource estimates for Llaguen as of January 1, 2026 are summarized below.

| Llaguen Mineral Resource Estimates1,2,3,4,5,6 |

Metric Tonnes | Cu (%) | Mo (g/t) | Au (g/t) | Ag (g/t) | CuEq (%) |

| Indicated Global (>= 0.14% Cu) |

271,000,000 | 0.33 | 218 | 0.033 | 2.04 | 0.42 |

| Including Indicated High-grade (>= 0.30% Cu) |

113,000,000 | 0.49 | 261 | 0.046 | 2.73 | 0.60 |

| Inferred Global (>= 0.14% Cu) |

83,000,000 | 0.24 | 127 | 0.024 | 1.47 | 0.30 |

| Including Inferred High-grade (>= 0.30% Cu) |

16,000,000 | 0.45 | 141 | 0.038 | 2.60 | 0.52 |

Note: totals may not add up correctly due to rounding.

1 CIM definitions were followed for the estimation of mineral resources. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

2 Mineral resources are reported within an economic envelope defined by a pit shell optimization algorithm. This pit shell is defined by a revenue factor of 0.33 assuming operating costs adjusted from Hudbay’s Constancia open pit operation.

3 Long-term metal prices of $3.60 per pound copper, $11.00 per pound molybdenum, $1,650 per ounce gold and $22.00 per ounce silver were used for the estimation of mineral resources.

4 Metal recovery estimates assume that this mineralization would be processed at a combination of facilities, including copper and molybdenum flotation.

5 Copper-equivalent (“CuEq”) grade is calculated assuming 85% copper recovery, 80% molybdenum recovery, 60% gold recovery and 60% silver recovery.

6 Specific gravity measurements were estimated by industry standard laboratory measurements.

Flin Flon Tailings Reprocessing

Hudbay is advancing studies to evaluate the opportunity to reprocess Flin Flon tailings where more than 100 million tonnes of tailings have been deposited for over 90 years from the mill and the zinc plant. The studies are evaluating the potential to use the existing Flin Flon concentrator, which is currently on care and maintenance after the closure of the 777 mine in 2022, with flow sheet modifications to reprocess tailings to recover critical minerals and precious metals while creating environmental and social benefits for the region. The Company is completing metallurgical test work and an early economic study to evaluate the tailings reprocessing opportunity and intends to initiate pre-feasibility studies in 2026.

- Zinc plant tailings – Hudbay operated a hydrometallurgical zinc facility where high grade critical minerals and precious metals were deposited for more than 25 years. Metallurgical test work continues following positive results from the initial confirmatory drill program completed in 2024. The results confirmed the grades of precious metals and critical minerals previously estimated from historical zinc plant records. An early economic study to evaluate the opportunity to reprocess the zinc plant tailings has confirmed the potential for a technically viable reprocessing alternative, and further engineering work is underway.

- Mill tailings – Initial confirmatory drilling completed in 2022 indicated higher zinc, copper and silver grades than predicted from historical mill records while confirming the historical gold grade. The tailings reprocessing opportunity is expected to reduce acid-generating properties of the tailings, which would improve the environmental impacts through higher quality water in the tailings facility and reduce the need for long-term water treatment. Additional work is underway to determine the reprocessing methodology and economic viability.

Qualified Person and NI 43-101

The technical and scientific information in this news release related to the Constancia mine, Snow Lake operations and Copper World project has been approved by Olivier Tavchandjian, P. Geo., Senior Vice President, Exploration and Technical Services. The technical and scientific information in this news release related to the Copper Mountain mine has been approved by Marc-Andre Brulotte, P. Geo., Executive Director, Global Mineral Resource Evaluation. Messrs. Tavchandjian and Brulotte are qualified persons pursuant to NI 43‑101 (as defined below). Additional details on the Company’s material mineral properties, including a year-over-year reconciliation of reserves and resources, are included in Hudbay’s Annual Information Form for the year ended December 31, 2025 (the “AIF”), a copy of which will be made available on SEDAR+ at www.sedarplus.ca and EDGAR at www.sec.gov.

The Mason PEA is preliminary in nature, includes inferred resources that are considered too speculative to have the economic considerations applied to them that would enable them to be categorized as mineral reserves and there is no certainty the preliminary economic assessments will be realized.

Supplemental Information for Talbot Drill Holes

| Talbot Deposit 2025 Drill Hole ID1,2,3,4 | From (m) | To (m) |

Intercept (m) |

Estimated true width (m) |

Cu (%) | Au (g/t) | Ag (g/t) | Zn (%) | CuEq (%) |

| TLS024 | 1556.0 | 1567.5 | 11.5 | 10.4 | 2.4 | 1.8 | 55.1 | 0.8 | 4.2 |

| TLS025 top | 1435.3 | 1449.5 | 14.2 | 13.2 | 1.2 | 0.8 | 17.8 | 0.5 | 2.0 |

| TLS025 bottom | 1459.0 | 1465.0 | 6.0 | 5.6 | 2.0 | 0.7 | 16.9 | 0.5 | 2.6 |

| TLS026 | 1265.5 | 1273.4 | 7.8 | 7.1 | 1.4 | 0.9 | 18.4 | 0.3 | 2.2 |

| TLS027W02 | 1252.8 | 1271.5 | 18.8 | 16.3 | 1.4 | 0.8 | 18.9 | 1.3 | 2.4 |

1. True widths are estimated based on drill angle and intercept geometry of mineralization.

2. All copper, gold and silver values are uncut.

3. Copper-equivalent (“CuEq”) grade calculated using the following long-term commodity price assumptions: $4.40 per pound copper, $2,800 per ounce gold, $32.00 per ounce silver and $1.25 per pound zinc.

4. Using the combined recoveries of New Britannia and Stall mills of 89% copper, 89% gold, 81% silver and 84% zinc.

| Talbot Deposit Hole ID |

From | To | Azimuth at intercept |

Dip at intercept |

||||

| Easting | Northing | Elevation | Easting | Northing | Elevation | |||

| TLS024 | 458,517 | 5,997,397 | -1,196 | 458,512 | 5,997,399 | -1,206 | 297.7 | -64.3 |

| TLS025 top | 458,301 | 5,996,995 | -1,097 | 458,296 | 5,996,997 | -1,110 | 291.8 | -68.0 |

| TLS025 bottom | 458,293 | 5,996,998 | -1,119 | 458,291 | 5,996,999 | -1,124 | 291.7 | -67.9 |

| TLS026 | 458,322 | 5,997,184 | -906 | 458,318 | 5,997,185 | -913 | 282.2 | -64.2 |

| TLS027W02 | 458,241 | 5,997,008 | -881 | 458,233 | 5,997,012 | -898 | 297.0 | -60.2 |

Note to United States Investors

This news release has been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of United States securities laws. Canadian reporting requirements for disclosure of mineral properties are governed by the Canadian Securities Administrators’ National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”).

For this reason, information contained in this news release containing descriptions of the Company’s mineral deposits may not be comparable to similar information made public by United States companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder. For further information on the differences between the disclosure requirements for mineral properties under the United States federal securities laws and NI 43-101, please refer to the Company’s AIF, a copy of which will be filed under Hudbay’s profile on SEDAR+ at www.sedarplus.ca and the Company’s Form 40-F, a copy of which will be filed under Hudbay’s profile on EDGAR at www.sec.gov.

Forward-Looking Information

This news release contains forward-looking information within the meaning of applicable Canadian and United States securities legislation. Forward-looking information is not, and cannot be, a guarantee of future results or events. Forward-looking information is based on, among other things, opinions, assumptions, estimates and analyses that, while considered reasonable by the Company at the date the forward-looking information is provided, inherently are subject to significant risks, uncertainties, contingencies and other factors that may cause actual results and events to be materially different from those expressed or implied by the forward-looking information.

Forward-looking information includes, but is not limited to, statements with respect to the Company’s production, cost and capital and exploration expenditure guidance, expectations regarding reductions in discretionary spending and capital expenditures, Hudbay’s ability to advance and complete the multi-year optimization of the Copper Mountain mine in British Columbia, including with respect to the primary SAG mill repairs and related ramp-up plans, the implementation of stripping strategies and the expected benefits therefrom, the expected timing and benefits of British Columbia growth initiatives, including with respect to the development timelines associated with New Ingerbelle and any challenges to the New Ingerbelle permits (including the LSIB’s recent application for judicial review), the estimated timelines and pre-requisites for sanctioning the Copper World project, including the completion and anticipated results of the definitive feasibility study and the potential timing of a project sanctioning decision, the expected benefits of the sanctioning of the Copper World project, the ability for Hudbay to complete mill throughput enhancements at its operating business units in Peru, British Columbia and Manitoba, the expected benefits of Manitoba growth initiatives, including the use of the exploration drift at the 1901 deposit, the potential utilization of excess capacity at the Stall mill, and the advancement of Hudbay’s exploration partnership with Marubeni Corporation (“Marubeni”) and Japan Organization for Metals and Energy Security (“JOGMEC”), in Manitoba, the anticipated use of proceeds from financing transactions, the Company’s deleveraging strategies and its ability to repay debt as needed including but not limited to with respect to the upcoming maturity of the 2026 Notes, expectations with respect to the timing and ability to satisfy the conditions required to close the acquisition of Arizona Sonoran Copper Company Inc. (the “ASCU Transaction”) and the expected benefits therefrom, expectations regarding the Company’s cash balance and liquidity and related cash management strategies, expectations regarding Hudbay’s capital planning strategies, including but not limited to Hudbay’s enhanced Capital Allocation Framework, expectations regarding the ability to conduct exploration work and execute on exploration programs on its properties and to advance related drill plans, including the advancement of the exploration program at Maria Reyna and Caballito and the status of the related drill permit application process, expectations regarding the Company’s ability to further reduce greenhouse gas emissions, Hudbay’s evaluation and assessment of opportunities to reprocess tailings using various metallurgical technologies, expectations regarding the prospective nature of the Maria Reyna and Caballito properties, the anticipated impact of brownfield and greenfield growth projects on the Company’s performance, anticipated expansion opportunities and extension of mine life in Snow Lake and the Company’s ability to find a new anchor deposit near its Snow Lake operations, anticipated future drill programs and exploration activities and any results expected therefrom, the enhancement of stakeholder engagement and advancement of a pre-feasibility study and related test work at the Mason copper project in Nevada, anticipated mine plans, anticipated metals prices and the anticipated sensitivity of the Company’s financial performance to metals prices, events that may affect the Company’s operations and development projects, anticipated cash flows from operations and related liquidity requirements, the anticipated effect of external factors on revenue, such as commodity prices, estimation of mineral reserves and resources, mine life projections, reclamation costs, economic outlook, government regulation of mining operations, and business and acquisition strategies. Forward-looking information is not, and cannot be, a guarantee of future results or events. Forward-looking information is based on, among other things, opinions, assumptions, estimates and analyses that, while considered reasonable by the Company at the date the forward-looking information is provided, inherently are subject to significant risks, uncertainties, contingencies and other factors that may cause actual results and events to be materially different from those expressed or implied by the forward-looking information.

The material factors or assumptions that Hudbay has identified and were applied in drawing conclusions or making forecasts or projections set out in the forward-looking information include, but are not limited to:

- the ability to achieve production, cost and capital and exploration expenditure guidance;

- no significant interruptions to Hudbay’s operations due to social or political unrest in the regions the Company operates, including the navigation of the complex political and social environment in Peru;

- no interruptions to the Company’s plans for advancing the Copper World project, including with respect to any challenges to the Copper World permits;

- no interruptions to the Company’s plans for advancing New Ingerbelle, including with respect to any challenges to the new Ingerbelle permits;

- the Company’s ability to successfully complete the stabilization and optimization of the Copper Mountain operations, and develop and maintain good relations with key stakeholders;

- the ability to satisfy the conditions required to close the ASCU Transaction;

- the ability to execute on the Company’s exploration plans and to advance related drill plans;

- the ability to advance the exploration program at the Maria Reyna and Caballito properties;

- the success of mining, processing, exploration and development activities;

- the scheduled maintenance and availability of the Company’s processing facilities;

- the accuracy of geological, mining and metallurgical estimates;

- anticipated metals prices and the costs of production;

- the supply and demand for metals the Company produce;

- the supply and availability of all forms of energy and fuels at reasonable prices;

- no significant unanticipated operational or technical difficulties;

- the execution of the Company’s business and growth strategies, including the success of its strategic investments and initiatives;

- the availability of additional financing, if needed;

- the ability to deleverage and repay debt, as needed including but not limited to with respect to the upcoming maturity of the 2026 Notes;

- the ability to complete project targets on time and on budget and other events that may affect the Company’s ability to develop its projects;

- the timing and receipt of various regulatory and governmental approvals;

- the availability of personnel for the Company’s exploration, development and operational projects and ongoing employee relations;

- maintaining good relations with the employees at the Company’s operations;

- maintaining good relations with the labour unions that represent certain of the Company’s employees in Manitoba and Peru;

- maintaining good relations with the communities in which the Company operates, including the neighbouring Indigenous communities and local governments;

- no significant unanticipated challenges with stakeholders at the Company’s various projects;

- no significant unanticipated events or changes relating to regulatory, environmental, health and safety matters;

- no contests over title to the Company’s properties, including as a result of rights or claimed rights of Indigenous peoples or challenges to the validity of the Company’s unpatented mining claims;

- the timing and possible outcome of pending litigation and no significant unanticipated litigation;

- certain tax matters, including, but not limited to current tax laws and regulations, changes in taxation policies and the refund of certain value added taxes from the Canadian and Peruvian governments; and

- no significant and continuing adverse changes in general economic conditions or conditions in the financial markets (including commodity prices and foreign exchange rates).

The risks, uncertainties, contingencies and other factors that may cause actual results to differ materially from those expressed or implied by the forward-looking information may include, but are not limited to, risks related to the LSIB’s application for judicial review of the regulatory decision to issue the New Ingerbelle permit amendment and the potential for it to have an adverse impact on the Company’s plans for the New Ingerbelle project, risks related to failure to effectively advance and complete the multi-year optimization of the Copper Mountain mine operations including with respect to the primary SAG mill repairs and related ramp-up plans, political and social risks in the regions the Company operates, including the navigation of the complex political and social environment in Peru, risks generally associated with the mining industry and the current geopolitical environment, including fluctuations in commodity prices, the potential implementation or expansion of tariffs, currency and interest rate fluctuations, energy and consumable prices, supply chain constraints and general cost escalation in the current inflationary environment, uncertainties related to the development and operation of the Company’s projects, the risk of an indicator of impairment or impairment reversal relating to a material mineral property, risks associated with the development of new projects, risks associated with acquisitions, investments and other strategic transactions including but not limited to the ASCU Transaction, risks related to the Copper World project, including the risk of capital cost escalation, permitting challenges, project delivery risks, and financing risks, risks related to the Lalor mine plan, including the ability to convert inferred mineral resource estimates to higher confidence categories, dependence on key personnel and employee and union relations, risks related to political or social instability, unrest or change, risks in respect of Indigenous and community relations, rights and title claims, operational risks and hazards, including the cost of maintaining and upgrading the Company’s tailings management facilities and any unanticipated environmental, industrial and geological events and developments and the inability to insure against all risks, failure of plant, equipment, processes, transportation and other infrastructure to operate as anticipated, compliance with government and environmental regulations, including permitting requirements and anti-bribery legislation, depletion of the Company’s reserves, volatile financial markets and interest rates that may affect the Company’s ability to obtain additional financing on acceptable terms, the failure to obtain or maintain required permits or approvals from government authorities on a timely basis, uncertainties related to the geology, continuity, grade and estimates of mineral reserves and resources and the potential for variations in grade and recovery rates, uncertain costs of reclamation activities, the Company’s ability to comply with its pension and other post-retirement obligations, the Company’s ability to abide by the covenants in its debt instruments and other material contracts, liquidity risks and its ability to access capital on acceptable terms, tax refunds, hedging transactions, cybersecurity risks and risks related to the reliability and security of the Company’s information technology and operational technology systems, including risks arising from cyber attacks, ransomware, phishing and other malware, risks associated with the use of artificial intelligence technologies, operational disruptions arising from environmental events such as wildfires or other forms of extreme weather, as well as the risks discussed under the heading “Risk Factors” in Hudbay’s most recent Annual Information Form and under the heading “Financial Risk Management” in the Company’s management’s discussion and analysis for the year ended December 31, 2025 which are available on the Company’s SEDAR+ profile at www.sedarplus.ca and the Company’s EDGAR profile at www.sec.gov.

Should one or more risk, uncertainty, contingency or other factor materialize or should any factor or assumption prove incorrect, actual results could vary materially from those expressed or implied in the forward-looking information. Accordingly, you should not place undue reliance on forward-looking information. Hudbay does not assume any obligation to update or revise any forward-looking information after the date of this news release or to explain any material difference between subsequent actual events and any forward-looking information, except as required by applicable law.

About Hudbay

Hudbay (TSX, NYSE: HBM) is a copper-focused critical minerals mining company with three long-life operations and a world-class pipeline of copper growth projects in tier-one mining jurisdictions of Canada, Peru and the United States.

Hudbay’s operating portfolio includes the Constancia mine in Cusco (Peru), the Snow Lake operations in Manitoba (Canada) and the Copper Mountain mine in British Columbia (Canada). Copper is the primary metal produced by the Company, which is complemented by meaningful gold production and by-product zinc, silver and molybdenum. Hudbay’s growth pipeline includes the Copper World project in Arizona (United States), the Mason project in Nevada (United States), the Llaguen project in La Libertad (Peru) and several expansion and exploration opportunities near its existing operations.

The value Hudbay creates and the impact it has is embodied in its purpose statement: “We care about our people, our communities and our planet. Hudbay provides the metals the world needs. We work sustainably, transform lives and create better futures for communities.” Hudbay’s mission is to create sustainable value and strong returns by leveraging its core strengths in community relations, focused exploration, mine development and efficient operations.

For further information, please contact:

Candace Brûlé

Senior Vice President, Capital Markets & Corporate Affairs

(416) 362-8181

investor.relations@hudbay.com

____________________

i Calculated using the mid-point of the annual guidance range.

ii Cash costs and sustaining cash costs are non-GAAP financial performance measures with no standardized definition under IFRS. For further details on why Hudbay believes cash costs are a useful performance indicator, please refer to the Company’s most recent management’s discussion and analysis for the period ended December 31, 2025.

iii The post-closing adjusted year-end cash and cash equivalents of $992 million includes December 31, 2025 cash and cash equivalents balance of $568.9 million and approximately $420 million of cash at the Copper World LLC level, which is designated for exclusive use by the Copper World joint venture. Post-closing adjusted liquidity includes the post-closing cash and cash equivalent plus the undrawn availability of $424.8 million under Hudbay’s revolving credit facilities.

iv For further information regarding the terms agreed to with Wheaton Precious Metals Corp. to enhance and amend the existing precious metals streaming agreement, please see Hudbay’s August 13, 2025 news release.

Figure 1: Regional Snow Lake Satellite Deposits

Hudbay increased its land package in Snow Lake by 250% in 2023, adding several regional satellite properties located within trucking distance of the Company’s processing infrastructure. The Company launched a significant geophysics program in 2024 and 2025 that included surface electromagnetic surveys using modern technology to target depths up to 1,000 metres. These efforts will continue in 2026 with the largest geophysics program in Hudbay’s history, including 600 kilometres of ground electromagnetic surveys and an extensive airborne geophysics survey.

Figure 2: Talbot Copper-Gold-Zinc Project

Talbot is a copper-zinc-gold rich VMS deposit located within trucking distance of existing processing infrastructure in Snow Lake. Hudbay commenced an extensive summer drilling program at Talbot in 2025 focused on expanding the known mineralization at depth, testing geophysical targets and conducting an infill drill program in the upper portion of the orebody. As part of the initial drilling program in 2025, Hudbay drilled five holes to test the continuity of the Talbot deposit at depth, with all holes intersecting intervals of copper mineralization. Assay results for TLS035 (in green) are currently pending.

Photos accompanying this announcement are available at https://www.globenewswire.com/NewsRoom/AttachmentNg/411d342a-8148-4b27-88b9-38a26aabc503

https://www.globenewswire.com/NewsRoom/AttachmentNg/240f6a35-19dc-4930-9b2b-fe8e9f4645ea

![]()