BIRMINGHAM, Ala., May 19, 2026 (GLOBE NEWSWIRE) — Forager Capital Management, the largest shareholder of Repay Holdings Corporation (NASDAQ: RPAY) (the “Company”), with beneficial ownership of approximately 13% of the issued and outstanding shares, sent the below open letter to stockholders of the Company.

May 18, 2026

Dear Repay Stockholders,

We are writing to inform you that the Board of Directors (the “Board”) of Repay Holdings Corp. (“Repay” or the “Company”) continues to refuse any meeting regarding our all-cash offer to purchase all outstanding common stock of Repay at $4.80 per share.

We were not surprised by the Board’s initial response. Directors asked to evaluate a transaction that could eliminate their roles are placed in a difficult and conflicting position. Saying “no” is easy. Delaying is easy. In many situations, buyers eventually lose interest, move on, and the status quo prevails.

Saying “no” is even a reasonable first step for a Board attempting to negotiate better terms for stockholders. But refusing to meaningfully engage with a buyer offering a 75% premium all-cash proposal suggests the Board is more focused on avoiding a transaction to preserve its positions than determining whether a superior outcome is achievable for stockholders.1 How can the Board credibly claim it is acting in your best interests when it has refused to determine whether additional value, better terms, or other protections may be attainable through engagement?

The Board provided no arithmetic or economic justification, just a conclusory rejection with boilerplate references to long-term value. The Board’s subsequent refusal to meaningfully engage now materially changes how stockholders should view the motive behind the rapid implementation of the poison pill.

Evaluation of this conduct will not be limited only to Repay stockholders. Institutional investors and proxy advisors pay close attention when directors adopt defensive measures without stockholder approval and then refuse to substantively engage on credible, premium offers. One of Repay’s own stockholders maintains a publicly stated policy of opposing directors who adopt poison pills without stockholder approval. These governance decisions will carry implications beyond this boardroom.

Because the Board’s response ultimately amounts to some variation of “trust us,” we believe stockholders should review the economic reality and historical record to decide whether that trust is justified.

KUBRA Transaction Belies Board’s Claim that $4.80 is “Significantly Undervalued”

The Board stated our $4.80 per share proposal “significantly undervalued” the business to such a degree that it didn’t even warrant a meeting. Yet the math underlying the Board’s own capital allocation decisions directly contradict that conclusion. Today, Repay can repurchase its own shares in the public market at $3.47 per share, nearly a 40% discount to the supposedly “significantly undervalued” price of $4.80.2 Instead of repurchasing Repay common stock, however, the Board chose to commit $372 million to the KUBRA acquisition despite Repay’s entire market capitalization being only $305 million.

Repay has stated that KUBRA will only be 25% free-cash-flow accretive, and not until 2028. Using the midpoint of Repay’s 2026 adjusted EBITDA guidance and Repay’s 45% free-cash-flow conversion target, that implies roughly $16 million of incremental free cash flow by 2028. On a $372m purchase price, that equates to only a 4% yield. And that comes only after years of integration, leverage, synergy assumptions, and execution risk.

By comparison, every dollar used to repurchase Repay common stock at the current trading price would imply nearly 40% upside just to reach our existing proposal price of $4.80 per share. That comes with no execution risk.

The Board’s position cannot be reconciled with its capital allocation decisions: if $4.80 is truly “significantly undervalued,” then repurchasing Repay shares at $3.47 is mathematically a better investment than KUBRA.

Repay Stockholders Have Seen This Movie Before

This is not the first time the Board has asked stockholders to trust its judgment regarding strategic alternatives. Repay announced a strategic review in March 2025 when the stock was trading around $7 per share. The Board ultimately chose not to pursue a transaction. Before our proposal became public approximately thirteen months later, the stock had declined to approximately $2.30 per share.

That outcome was no accident. Since Repay became a public company on July 11, 2019, the Company has completed eight acquisitions with aggregate announced value of approximately $912.5 million: TriSource, APS Payments, Ventanex, cPayPlus, CPS Payment Services, BillingTree, Kontrol, and Payix. That figure excludes the pending $372 million KUBRA acquisition.

Yet today, Repay’s entire enterprise value is only $673 million (excluding the tax receivable agreement liability, and $865 million if including that liability). That figure reflects the value of the entire Company, not just the acquired assets. In other words, the Board has already spent $912.5 million on acquisitions even though the entire enterprise is worth only $673 million today. This is not the track record of a Board that has earned the right to ask stockholders to sign up for the sequel.

Stockholders Consistently Left Behind

Repay’s total stockholder return has substantially underperformed the peer group selected by the Board itself in the Company’s own proxy disclosures:

That naturally leads to a broader question: has this Board earned the level of deference it is now demanding from stockholders? We are not here to drag individual directors through the mud. In fact, we repeatedly attempted to meet privately with the Board to avoid a public dispute like this altogether. But the Board rejecting a 75% premium all-cash offer without meaningful engagement inevitably places its own judgment and track record under scrutiny.

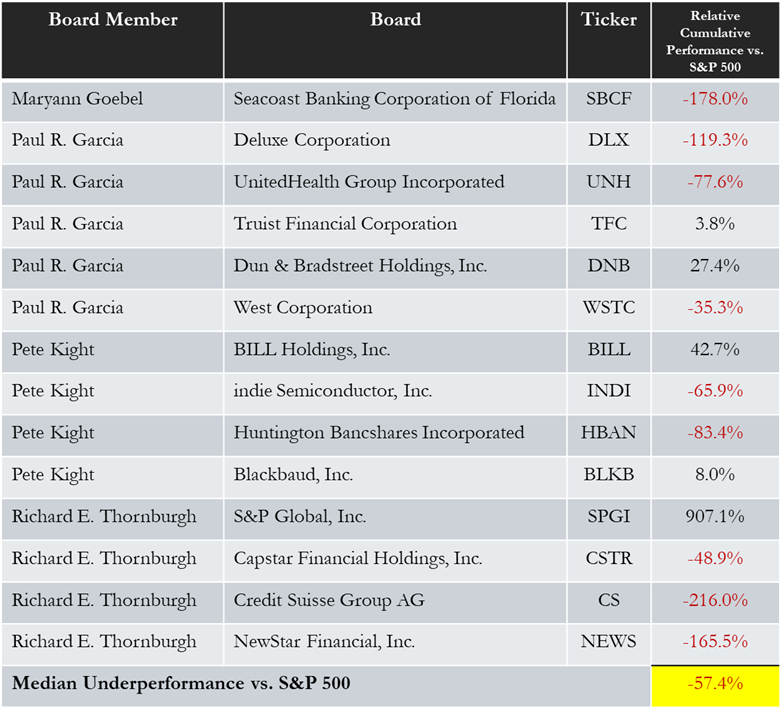

Collectively, Paul Garcia, Maryann Goebel, Pete Kight, and Richard Thornburgh have served on 14 outside public company boards over the course of the last ten years (tickers: SBCF, DLX, UNH, TFC, DNB, WSTC, BILL, INDI, HBAN, BLKB, SPGI, CSTR, CS, and NEWS). Across those board tenures, the median cumulative performance trailed the S&P 500 by approximately 57%.

These are not the results that earn blind trust from stockholders.

We Remain Committed at $4.80

We obviously like the Company and its employees. Our $4.80 per share offer remains outstanding and actionable.

Rather than meaningful engagement regarding a 75% premium all-cash offer, the Board has decided for you that stockholders should once again trust a historical record that has failed to create value.

Stockholders should ask a few simple questions: Why is the Board so unwilling to engage? Why was a poison pill adopted so quickly without stockholder vote before substantive engagement occurred? Why was the KUBRA transaction announced after the stockholder nomination window closed? Why is Repay not repurchasing shares at $3.47 per share rather than acquiring KUBRA if $4.80 is so significantly undervalued?

We remain ready to engage immediately. Our advisors and counsel are prepared to begin diligence and negotiate a transaction document. Stockholders should expect meaningful engagement and a credible explanation for why that engagement has been refused.

Sincerely,

Forager Capital Management

1 Forager’s original proposal offered $4.80 per share in cash. Based on Repay’s 30-trading-day volume-weighted average price of approximately $2.74 through the close on April 15, 2026, the proposal implied a premium of approximately 75% (($4.80 / $2.74) – 1 = 75.2%).

2 Repay’s May 15, 2026 closing price of $3.47, the proposal implied a premium of approximately 38.3% (($4.80 / $3.47) – 1).

Photos accompanying this announcement are available at

https://www.globenewswire.com/NewsRoom/AttachmentNg/29266abb-6ee9-43c2-a557-04bafd90ea8e

https://www.globenewswire.com/NewsRoom/AttachmentNg/dc2e5e9e-b304-4a9d-92f8-a8e9c324ce78